China is hitting its climate targets years ahead of schedule

China’s 13th five-year plan is quite possibly the most important document in the world in setting the pace of acting on climate change.

With the first draft of the energy sector plan likely released in June, and the overarching strategy intriguingly promising to ‘enhance’ its climate contributions, the stakes are high.

However, the kind of climate action once expected to be laid out in the plan is actually already taking place in the real world.

Clean energy deployment is exceeding targets.

The structure of the economy is changing rapidly, with services and private consumption – sectors with very low energy intensity in relative terms – growing while the heavy industry sectors responsible for most of the coal consumption and CO2 emissions are contracting.

As a result we are seeing falling carbon emissions — and more blue skies.

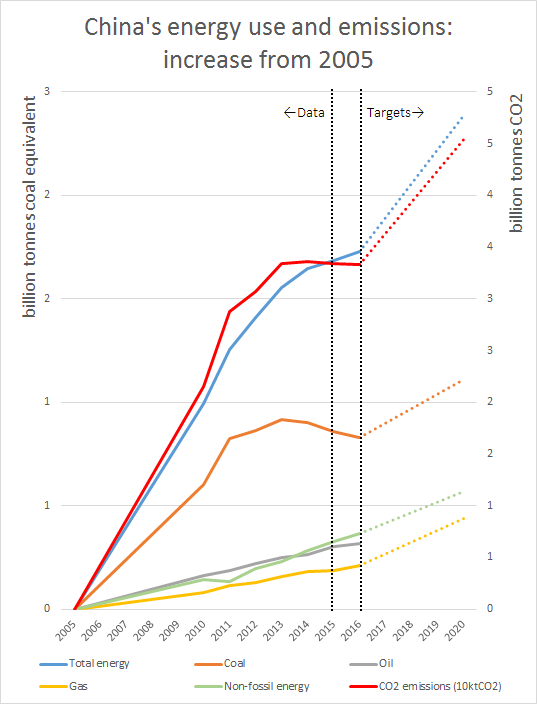

The speed of change

China’s National Energy Agency’s workplan for 2016 implies that coal use will fall and CO2 emissions will flatline this year.

This is the first time that the new trends have been incorporated into official projections.

The speed of structural change appears, however, to have taken the central planning apparatus completely by surprise.

2020 energy targets that would have seemed quite meaningful or even ambitious a few years ago have now become redundant.

The share of coal in the total energy mix will fall below 63% already this year, having fallen one percentage point per year since 2010.

The current target for 2020 is 62%, meaning that this target will probably be met in 2016 or 2017 — up to 4 years in advance.

The total installed capacity of wind and solar reached 180GW in 2015, against a target of 140GW.

Annual installations were 46GW, meaning that the current 2020 target of 300GW will be reached two and half years in advance, by mid-2018, just by maintaining the current rate.

All additional power demand is being met with clean energy, meaning that fossil fuel fired power generation will keep falling.

Just the beginning

Growth in coal use and CO2 emissions has been cooling down since 2011, and 2016 will almost certainly be the third year in a row that coal consumption falls in absolute terms.

Yet the current official targets, dating back to 2014, seek to “limit” coal use growth to 3% per year, a rate that has not been seen since 2011 and will in all likelihood not be seen ever again for a sustained period of time.

Furthermore, the fundamental shift in China’s economic structure has barely started, with the full transition from debt-fueled capital spending to private consumption as the key driver likely to take at least a decade.

2020 CO2 emissions and coal use are likely to be at least 10% below the targets set in 2014.

A key dilemma for energy planners is that targets for total energy consumption and CO2 emissions were already set in the overarching five-year plan released in March, and these targets do not yet take into account the dramatic shifts that have taken place in the past few years.

All of this means that China’s coal use and CO2 emissions are going to keep falling much sooner and faster than anyone anticipated.

It also means that the government has very significant scope to step up the targets and accelerate the trends.